The risk layer your vendor risk management is missing.

Cyber ratings tell you if a vendor can be hacked. We tell you if they will remain solvent. Continuous vendor financial risk monitoring, powered by AI research agents.

Trusted by:

Most TPRM tools were built for cyber and compliance. They run questionnaires, check SOC 2 reports, and score attack surface. None of that tells you whether your supplier is six months from Chapter 11. When a critical vendor goes under, the damage isn't theoretical — it's missed shipments, failed audits, and an emergency rebid.

STALE QUESTIONNAIRES

Annual questionnaires go stale the day you send them.

CYBER RATINGS MISS FINANCIAL DISTRESS

Cyber ratings don't cover financial distress.

SPREADSHEETS DON'T SCALE

SPREADSHEETS DON'T SCALE

Continuous vendor financial risk, on autopilot.

Minutes

100%

15

.avif)

Step 1: Connect your vendor list

Upload a CSV or sync from your ERP. We handle entity matching automatically.

LEARN MORE

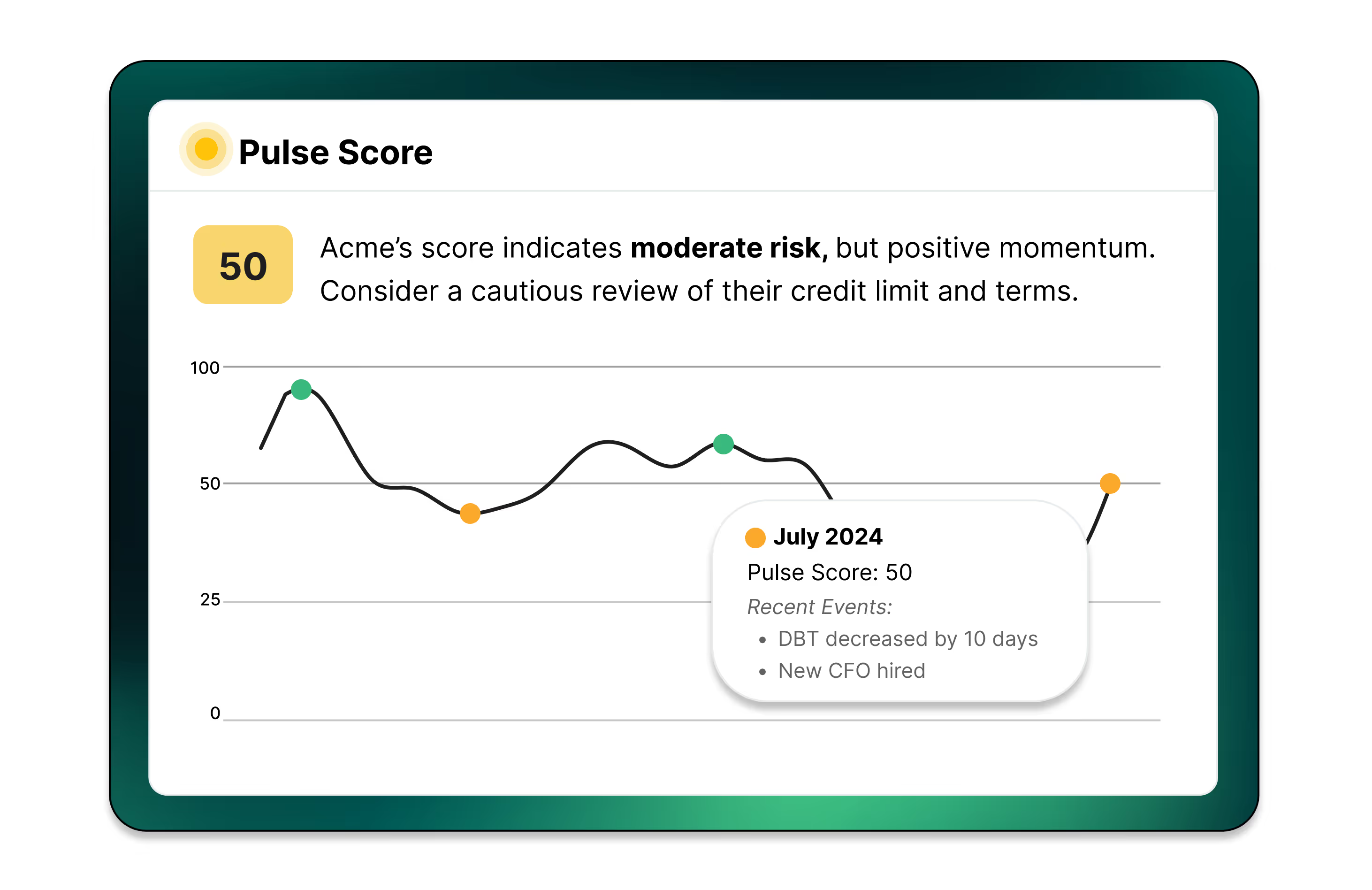

Step 2: We score every vendor

Our research agents pull financial signals, credit data, and public filings. You get a score and a written risk summary per vendor in minutes, not weeks.

LEARN MORE

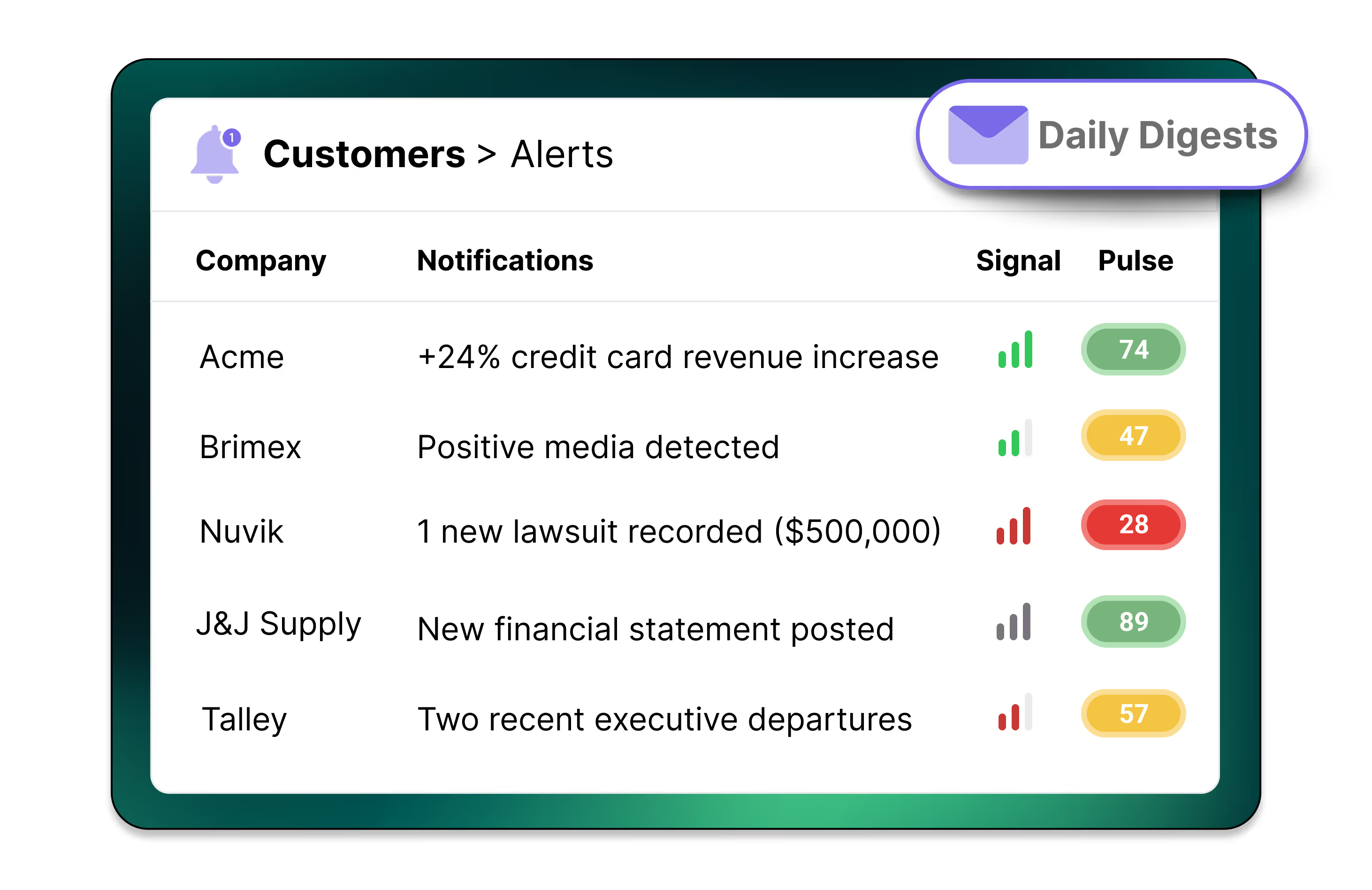

Step 3: We monitor every vendor

Don't guess with vendors. Credit Pulse monitors your entire portfolio for emerging supply chain risk.

LEARN MORE

Ready to modernize credit for your SaaS business?

.webp)

Nathan Rugg

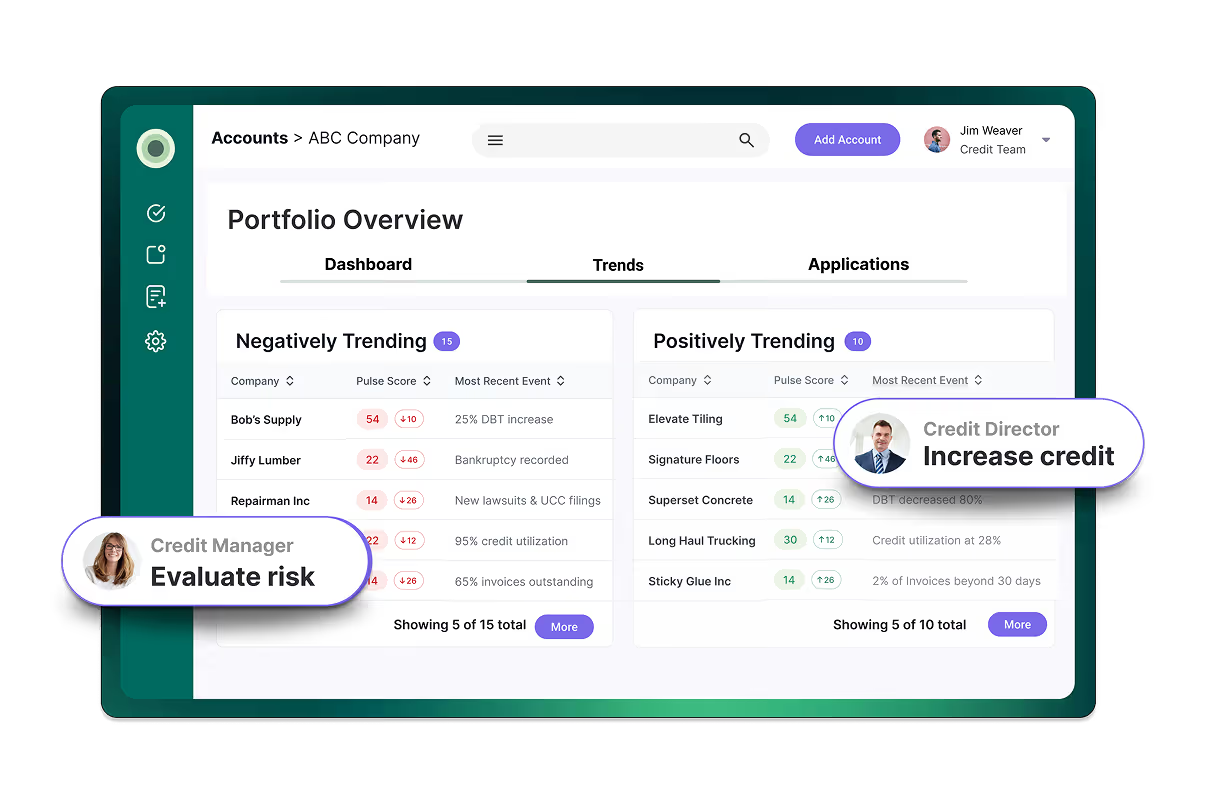

For Matrix Adhesives. managing credit across multiple operating companies created inconsistent processes, slower approvals, and limited visibility into portfolio risk. With Credit Pulse, they were able to:

- Standardize onboarding and monitoring across all operating companies

- Increase trade reference collection rates by 30%

- Reduce onboarding turnaround times by 65%

- Monitor customer risk changes with automated, signal-based alerts

.jpeg)

Andrew Ceccorulli

Laticrete needed to move faster without stretching a lean credit team even thinner. Manual onboarding and limited visibility into private contractors created delays across the business. With Credit Pulse, they were able to:

- Cut new customer decision times to as little as 15 minutes

- Avoid $160K in additional analyst hiring costs

- Accelerate millions in revenue through faster, standardized onboarding

James Kim

As product demand surged, Nowadays needed a faster way to evaluate and onboard new retail customers. Manual applications and limited visibility into smaller businesses slowed approvals and increased risk. With Credit Pulse, they were able to:

- Cut credit decision times by 50%

- Access 5x more data on small and independent retailers

- Reduce manual onboarding work with a digital credit application

Transform your credit process today.

Meet with our team or try us free for 30 days.